Introduction

For over 30 years Japan has defied the traditional laws of economics, maintaining a careful balancing act of curbing inflation cycles and rising rates that developed nations often struggle with. Japan’s economy has been notoriously unconventional, defined by deflation, low interest rates and near zero bond yields, trying to generate inflation and growth rather than manage it. But how exactly did Japan find themselves here and what does Japan’s economic resurgence mean for global markets?

Turbulent Beginnings

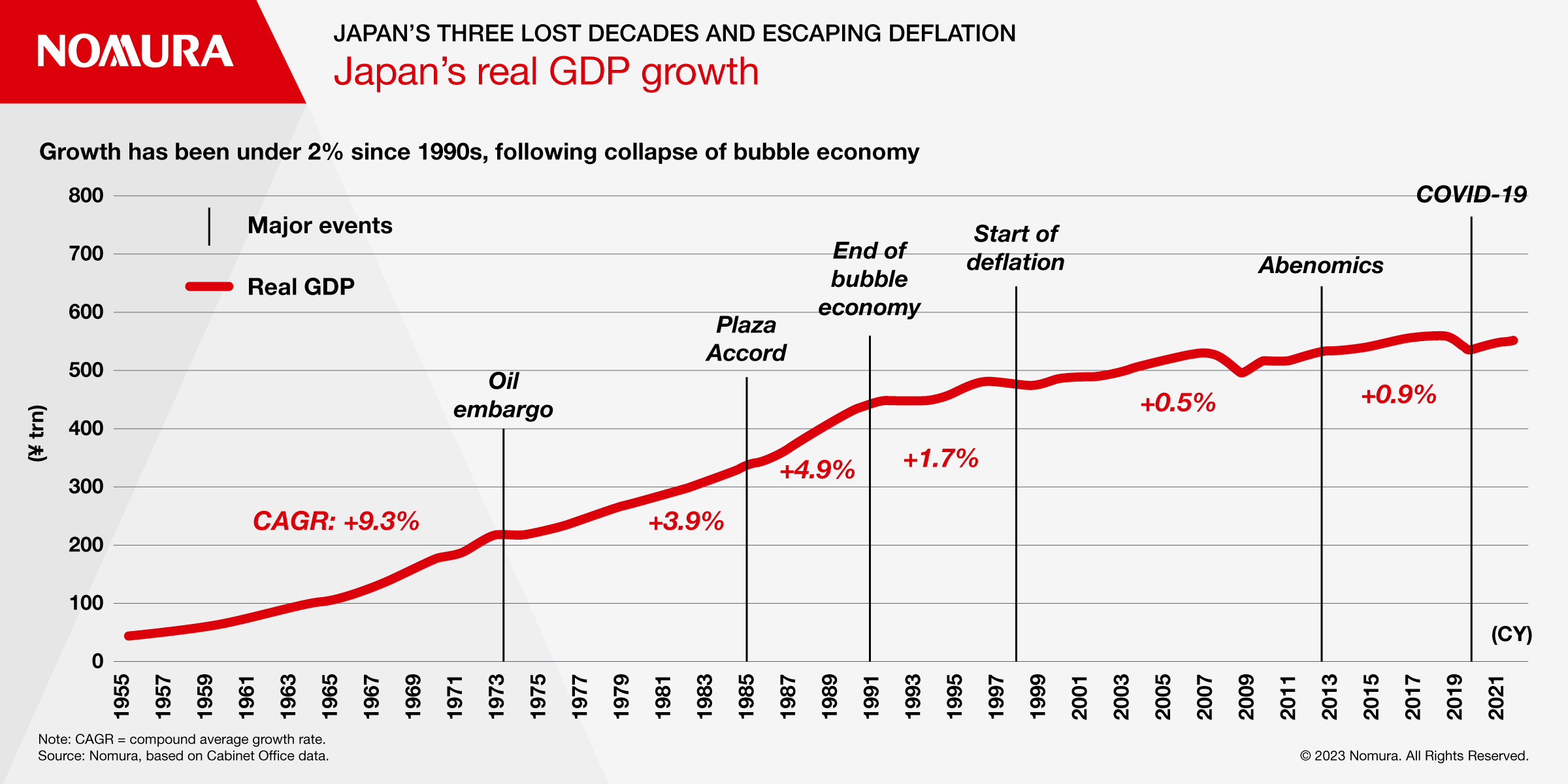

Following the conclusion of The Second World War, Japan’s economy under the Keiretsu system (Lume) experienced high growth, averaging 10.1% in the 1960s and 5% over the following two decades (Treasury). Peaking in 1989, the strong growth was linked with an asset price bubble which burst catastrophically in 1991, sending Japan’s economy spiralling into low growth and disinflation, recognised as the “Lost Decades.” Due to this significant weak growth, the economy soon fell into periods of disinflation, prompting the Bank of Japan (BoJ) to drop interest rates to near zero, a policy they maintained for the better part of three decades until very recently (Bank of Japan).

Japan’s Lost Decades, and Escape from Deflation (Source: Nomura)

Unconventional Liquidity Boost

The bond market in Japan was also lowered to near zero as the BoJ pioneered a quantitative easing system in 2001 to combat domestic disinflation (ox). The Bank bought up 47% of all Japanese Government Bonds (JGB) to increase liquidity in the economy (econ). The increased supply of cash placed downwards pressure on borrowing costs, and was designed to stimulate domestic investment, leading to the economic strength of the 70s and 80s which transformed the nation from a post-war industrial hub to a global trade and production superpower.

Higher Highs, Lower Lows

However, while the nation rode this wave of euphoria, they fell gradually into a liquidity trap, pinning the economy in stagflation for an entire generation. At the same time, near-zero rates led to the rise of the “yen carry trade”, where investors borrowed cheaply in yen to then reinvest in higher-yield assets overseas. It wasn’t until recent times where there has been a major shift within the Japanese economy, brought about by COVID, stagnant wage growth, surging energy prices and a weakening yen disrupting global supply chains. Inflation soon rose, followed by rates as investors demanded higher bond yields to compensate for losing purchasing power.

Weak domestic consumer demand and wage growth brought about deflation in 2021, before global disruptions pushed prices back up (Source: NovaScotia)

Japan remains one world’s largest economies and most significant bond markets. Thus, as cash rates and government bond yields begin rising after decades, the country is undergoing major economic and financial reforms. Given Japan is synonymous with near-zero cash rates and bond yields, this shift has implications not only on the domestic economy of Japan, but also the global financial markets and international capital flows.

Reckless Policy, or Calculated Risks?

Now, why was Japan’s monetary policy so loose? Throughout the 1990s, in an attempt to stimulate growth and transition out of the “lost decade”, the Japanese government increased spending and eased monetary policy. However, monetary policy proved to be largely ineffective, primarily due to late action and the existence of deflation causing what was perceived as a nominal rate cut, to in reality do little to bludgeon high real interest rates. As a result of the continued recession, Japan adopted close to zero interest rates, then transitioned to negative interest rates paired with quantitative easing. Instead of earning interest on savings, people would instead be charged to store their money in banks, incentivising expenditure, combatting deflation, and decreasing foreign demand for the yen in order to achieve depreciation which boosts exports.

Japan’s 10-year Government Bond yields have risen to record levels not seen this century (Source: LiveWireMarkets)

In March 2024, Bank of Japan had their first interest rate increase in 17 years, raising short term rates -0.1% to the 0-0.1% range, ending an 8-year stint of negative rates. Moreover, the Bank of Japan also abolished yield curve control, which capped long-term 10-year bond yields to zero, marking the end of their unconventional monetary policy strategies.

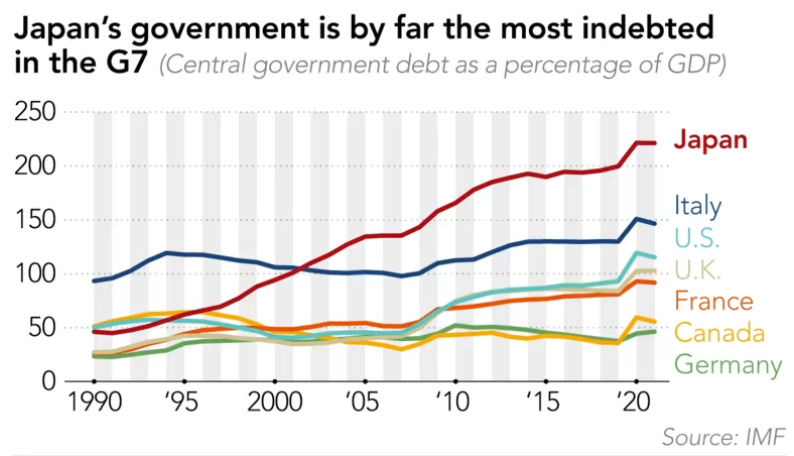

Initial fiscal policies revolved around public investment in roads and bridges to meet political commitments, rather than supporting consumption and investment expenditure. It was not until Shinzo Abe began spending to boost aggregate demand through targeted initiatives following his 2012 re-election. With this significant expenditure, Japan has accumulated a significant level of debt, with a staggering gross debt-to-GDP ratio of 204.4%. Comparatively, the US, branded as having a significant level of debt, appears less significant when paired against Japan, with a ratio of 125.8%. Further, the historical scars of prolonged deflation and fears of its recurrence are believed to still influence Japanese policymakers as they continue to be relaxed in their monetary policy settings, with relatively low rates compared to other nations despite rising inflationary pressures.

Japan consistently leads major nations in accumulated public debt (Source: NikkeiAsia)

Factors Triggering This Shift

So, what triggered this monetary policy shift? The decision was reasoned and motivated by the increased confidence by the central bank that Japan had “emerged from the grip of deflation” with inflation being above the target core CPI of 2% for well over a year. Since then, Japan has bucked their historical trends, with rising domestic inflation due to strong wage growth of 5.28% in 2024 and a depreciating yen, which caused continued annual inflation to be above target. As a result, the Bank of Japan continued to gradually increase interest rates, rising to its highest levels in 30 years to 0.75% in January 2026.

With recent rising inflationary pressures, this makes Japan’s long-term bonds appear less attractive, driving bond prices down and therefore increasing bond yields. Remember when the Bank of Japan abolished its yield curve control in 2024, targeting 0% yields on 10-year bonds with a cap of 1% or more. Since the removal, combined with continued growth and a rising price index, Japanese 10-year bond yields have surged, reaching a yield of 2.8% in May 2026, its highest level since 1996.

Global M&A and IB Activity

In 2024, the value of M&A deals involving a Japanese company rose 44% to more than $230 billion, the fastest growth since 2018, climbing to almost US$400 billion in 2025. Such growth can be attributed to the governance reform requested by the Tokyo Stock Exchange (TSE), resulting in a massive demand pipeline for restructuring and divestiture services within M&A advisory.

While higher rates compress LBO and other debt-financed acquisitions, companies with inefficient capital allocation and weak balance sheets can no longer survive on cheap debt, generating deal flow and advisory mandates for investment banks. In a traditionally low-rate environment like Japan, rate hikes are significant and beneficial for IB activity despite being headwinds for deal financing themselves.

Reliance on Hormuz

Additionally, the current conflict between Iran, the US and Israel has had major ramifications to Japan, contributing to higher inflation and higher yields. The conflict has led to the closure of the Strait of Hormuz, which serves as a critical waterway for Middle Eastern oil and LNG producers, seeing over 20 million barrels of oil and oil products pass through daily. Now, how would the closure impact Japan? The nation is heavily reliant on the Middle East imports of oil, contributing to over 90% of crude oil imports. With such a heavy reliance on energy imports, a supply shock from the war saw a rise in oil prices due to the uncertainty that had the impact of creating further inflationary pressures and circulating back into higher bond yields.

Future Outlook

Further, the sustained yen weakness and with oil prices surging by 7% in March, these expectations of higher inflation are expected to continue. A Bank of Japan survey indicated that 83% of consumers expect prices to continue to rise in the next 12 months, exemplifying expectations of a further rate hike from the Bank of Japan.

Conclusion

Japan’s economic story is one of the most consequential in modern financial history, as investors watch a 30-year structural reset from unconventional economics to deflation management to inflation control. Consequences may already be arriving. Bond yields at 30-year highs are repricing risk across global fixed income markets. A revitalised corporate governance framework is unlocking deal flow frozen inside Keiretsu structures for generations. Rising rates, while compressing leverage, are forcing the capital efficiency reckoning that activists and regulators have long demanded.

What remains uncertain is the pace. Every day of the Strait’s closure sustains inflationary pressure while the BoJ navigates rate normalisation against a debt-to-GDP ratio approaching 237%. The margin for policy error is narrow. The world will watch on as Japan walks the tightrope between economic normalisation and debt sustainability, driven by growth and wages.

The CAINZ Digest is published by CAINZ, a student society affiliated with the Faculty of Business at the University of Melbourne. Opinions published are not necessarily those of the publishers, printers or editors. CAINZ and the University of Melbourne do not accept any responsibility for the accuracy of information contained in the publication.