Introduction

In 1849, 300,000 hopeful prospectors chasing the Californian gold rush went broke, while the merchants who sold them the pickaxes, shovels, and denim trousers left filthy rich without panning an ounce. Today, parallels can be drawn in the race for artificial intelligence, except on an unimaginably larger scale.

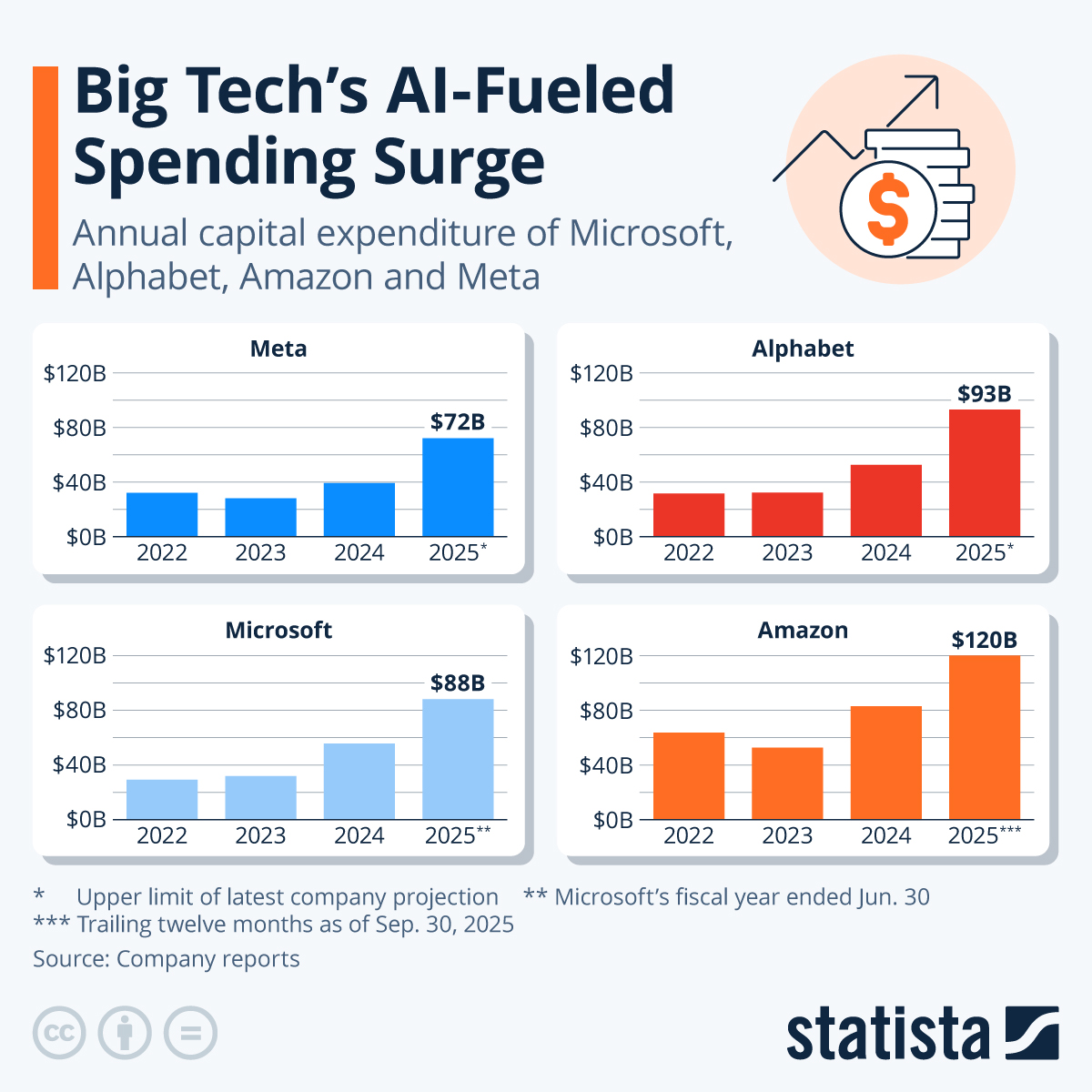

Amazon, Microsoft, Google, and Meta’s Q3 FY26 earnings showed us the constraint lies in supply, essentially arguing the faster they spend the faster they can monetise the demand out there. According to Futurum, these hyperscalers are projected to double the previous year’s expenditure, growing to almost US$700 billion on AI infrastructure in 2026 alone. While the world watches ChatGPT, Gemini, and Claude’s heavyweight titlefight for the smartest model, a much quieter group of companies sit ringside getting paid regardless of who wins.

Big Tech AI expenditure has increased exponentially over the last 5 years (Source: Statista)

Semiconductors and the Silicon Supply Chain

Everyone knows NVIDIA and AMD, the world’s premier chip designers. Fewer know their dependence on TSMC, the foundry powering 70% of the world’s pure-play semiconductor market. Even less appreciate the dependency these giants have on a much smaller and stranger Dutch company based out of Veldhoven.

ASML does not make chips. They specialise in lithography, making machines that direct light through a series of mirrors and lens to print circuit patterns onto impossibly small sub-3-nanometer silicon wafer chips, tech that no other company has been able to recreate. Every advanced AI chip can be traced to one of ASML’s systems. Each machine is the size of a double-decker bus, weighs as much as a blue whale, and uses a special type of light developed by ASML that does not naturally occur on Earth’s surface, known as extreme ultraviolet (EUV). Despite its $400 million price tag, hyperscalers wait for months to access this tech in their foundries, making the message clear: If you want to make a modern AI chip, you wait in ASML’s line.

ASML’s Lithography Machines (Source: Bloomberg)

Bespoke Silicon Solutions

AI isn’t a blanket coverage – Meta Ads, Google Search, every tech giant has carved out their own niche in this race for intelligence. While NVIDIA sells standardised GPUs, Broadcom and Marvell have silently captured 95% of the custom AI ASIC (Application-Specific Integrated Circuits) market. Every chip, known as “accelerators”, are co-designed with customers and custom-built for specific AI workloads rather than broad applications, resulting in massive cost-efficiency and superior performance-per-watt. They are “fabless”, meaning they simply design the chips before handing it over to TSMC for production. Broadcom designs Google’s TPU and OpenAI’s custom chips, targeting US$100 billion in annual AI chip revenue by 2027, and carries a $73 billion demand backlog. Marvell designs Amazon’s Trainium and Microsoft’s Maia, with projected revenues of US$11 billion and a reported US$2 billion investment from NVIDIA to integrate their designs into NVLink technology within data centres.

The hyperscaler “in-house silicon” race is, structurally, a duopoly as these designers embed themselves in a customer’s chip program for years. As TSMC’s capacity is projected to tighten, custom silicon becomes increasingly important. Pricing power grows with scarcity, and Broadcom and Marvell’s reserved capacity at the foundry perfectly positions them to benefit from the next CapEx wave.

Broadcom co-developed Google’s Revolutionary 7th Generation “Ironwood” TPUs (Source: The Wall Street Journal)

Bigger is Better?

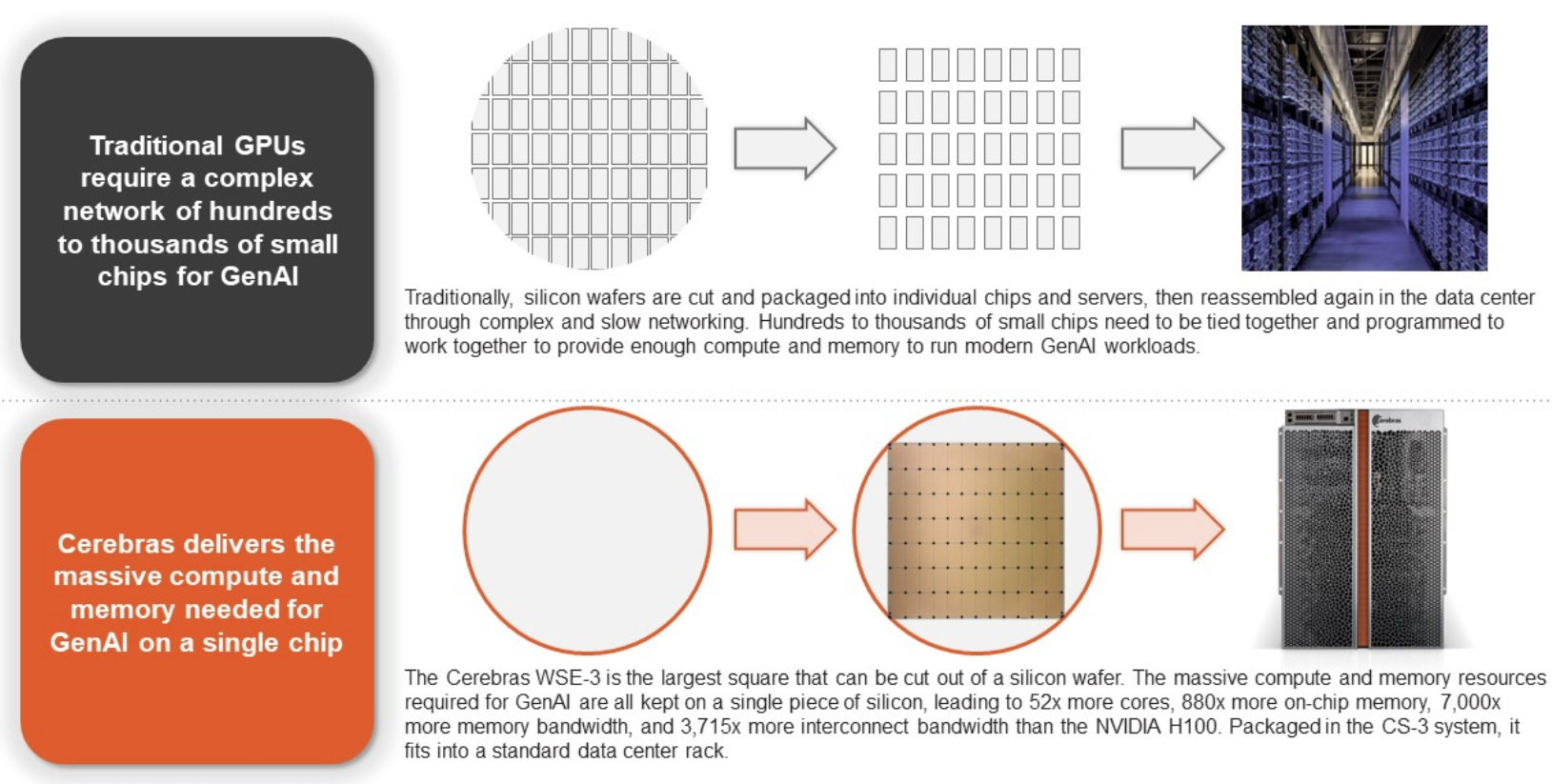

With a 20x oversubscribed IPO popping 89% on its NASDAQ debut to $95 billion cap, Cerebras has emerged as the hottest newcomer to this market. Rather than cutting silicon wafers into individual GPU dies and stitching them together with networking, Cerebras leaves the wafer whole. Its thesis suggests AI inference is becoming increasingly bottlenecked by memory bandwidth rather than raw compute, and that a single wafer removes the inter-chip communication requirements slowing GPU clusters down. Backed by AWS deployment alongside $20 billion agreements with OpenAI, Cerebras’ pitch is one that markets and hyperscalers are taking very seriously.

Cerebras’ whole wafer design reportedly produces up to 20x inference gains compared to NVIDIA GPUs (Source: The Motley Fool)

Memory Bottlenecks

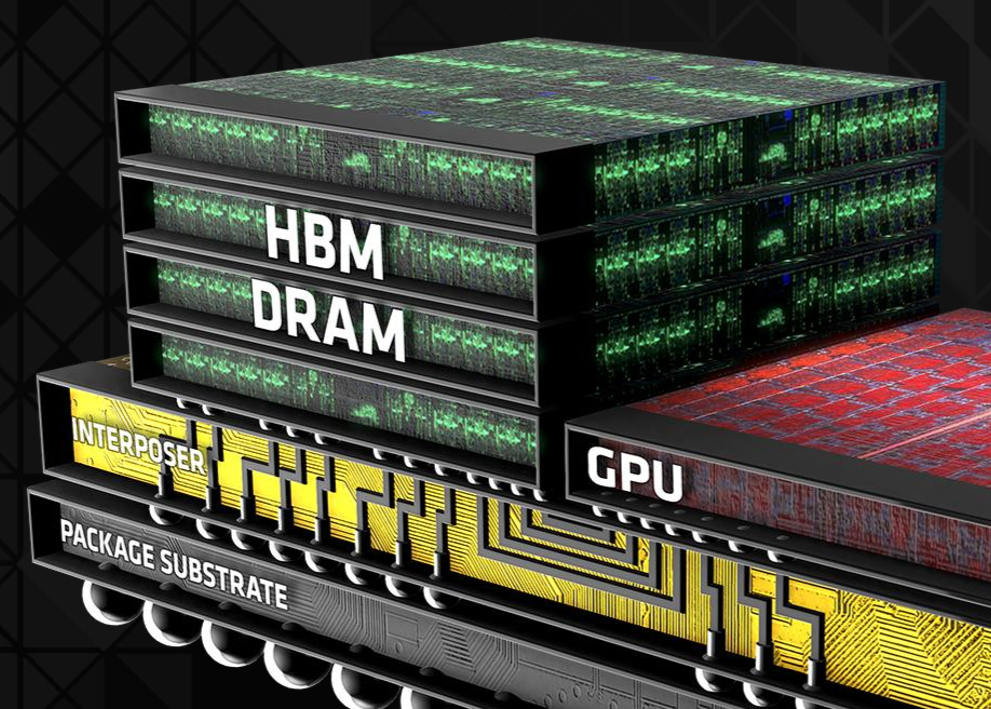

Data centres require thousands of GPUs powering their racks, which in turn require massive amounts of memory. Once a prompt is received and rerouted within the data centre, it is tokenised, transforming words into numbers that LLMs can process. These token IDs are sent into GPU memory, where billions of daily queries are processed and stored. Micron, SK Hynix, and Samsung control over 90% of this global memory market, known as dynamic random access memory (DRAM). GPUs use High Bandwidth Memory (HBM), which are vertically stacked smaller DRAM chips used to feed compute cores for inference within AI accelerators.

In many modern AI workloads, the limiting factor is no longer raw compute power, but memory. Data is being moved constantly across AI models, and the chips are processing it faster than memory systems can supply it. The memory shortage has been severe enough that, according to a Bloomberg report cited by Nasdaq, prices for one variety of DRAM rose 75% in a single month between December 2025 and January 2026.

Micron’s HBM fit alongside the data centre tech stack (Source: Tom’s Hardware)

GPUs and memory run hot, which is where Vertiv comes in. Vertiv makes the liquid cooling and power distribution systems inside the data centre itself, co-engineering thermal solutions for each new GPU reference architecture with NVIDIA themselves. The company reported a 252% year-on-year jump in orders as rack densities pushed past 100 kilowatts. Air cooling simply cannot keep up with the heat exhaust of top-tier tech, perfectly positioning Vertiv to capitalise and scale alongside demand.

Optical Networking and Photonics

As GPU clusters within data centres scale, a structural bottleneck emerges within the connecting copper wires as they are pushed to their physical limits in bandwidth, latency, and power consumption, not to mention the added strain on compute and memory. So is there something else we can use? NVIDIA’s US$4 billion investment seems to think so, securing multi-year purchase commitments and capacity rights in photonics companies Lumentum and Coherent in March 2026.

In short, data is encoded into photos within light and sent via pulses through optical transceivers and fibre, solving many of the concerns associated with heating, bandwidth, and signal degradation. Photonics has been deeply established for decades in telecom and long-haul networking, with hyperscalers repurposing this technology to essentially get their GPUs to exchange information quicker, more frequently, and reliably.

Lumentum specialises in lasers, specifically Indium Phosphide (InP) externally-modulated lasers (EML), which are notoriously difficult to work with. Their decades of refinement and expertise in manufacturing them at high yields, reliability, and scale remains unmatched by any competitor, with an estimated 50-60% share of the high-end EML market. These lasers sit in optical transceivers, small modules that translate between electrical data and light embedded in switches, servers, and GPU networking equipment, transmitting hundreds of gigabits per second. Coherent is the more diversified of the two, offering the complete optical system suite spanning networking, materials, and lasers. The Pennsylvania-based company produces everything from transceivers to co-packaged optics, enabling high-speed GPU connectivity within data-centre racks.

Lumentum’s industry-leading InP laser technology (Source: Seeking Alpha)

NVIDIA’s rationale is clear, aiming to leverage Lumentum’s expertise against Coherent’s broader tech stack to guarantee access and grow their overall silicon photonics ecosystem. Their respective stocks have rallied 1,169% and 375% over the last year as investors grow increasingly excited about optics scaling alongside compute.

The Real Estate Behind Cloud Compute and Orchestration

Once you have the chips, memory, power, and even photonics, you still need to assemble them into clusters within massive facilities. Major cloud providers like Amazon Web Services and Microsoft Azure already capture most of this general-purpose market, but a newer, more specialised group of providers have emerged. Known as neoclouds, these firms specifically rent out high-performance, purpose-built data centres to host, train, and run AI and machine learning workloads, reportedly achieving cost reductions of over 60%.

CoreWeave is the largest of the group, anchoring major tenants including Microsoft and OpenAI within its fleet of 100,000+ GPUs across 43 active data centres in the EU and US, holding enough contracted capacity to power over 24,000 racks or 1.7 million NVIDIA GPUs. Their three main customer segments are AI labs, enterprises integrating AI into workflows, and hyperscalers requiring overflow capacity. Revenue grew 168% YoY in 2025 and its demand backlog to US$66.8 billion, with the substantial majority of new 2026 capacity already under long-term commitments.

Another emerging name is Nebius, a Dutch challenger scaling GPU-dense capacity across the EU and US on the back of US$17.4 billion and US$27 billion deals with Microsoft and Meta respectively, and a US$2 billion equity investment from NVIDIA. While CoreWeave competes primarily on raw scale and proximity to the US hyperscaler market, Nebius is more vertically diversified, designing its own data centres, building its own racks, procuring its own compute, and deploying its own AI software layer with a strong focus on European data sovereignty.

Critics have branded these arrangements as “circular financing”. Coreweave needs capital to buy GPUs for its tech stack. NVIDIA invests $2 billion. Coreweave uses this to buy more NVIDIA GPUs. Revenues of both parties increase, NVIDIA’s investment appreciates, investors are happy, everyone wins. Such a pattern emerges across NVIDIA’s investments, targeting a specialist-generalist combination within newer segments in the data centre tech stack, securing long term equity agreements to grow compute capacity and revenues for both businesses. Circular deals inflating a bubble, or just smart business?

The picks and shovels building the AI tech stack (Source: Generative Value)

Conclusion

It’s easy to get lost in the trillions spent on AI, but the downside is very real. Investors may not see the already priced-in returns that they expect. The point of the picks-and-shovels frame is not risk immunity. It is that they are at least one step removed from the question of who wins, which model architecture dominates, or whether any specific consumer application takes off. ASML gets paid whether the chips power ChatGPT or Gemini. Broadcom makes chips for as long as people search on Google. Vertiv cools components regardless of whose they are.

Once the gold ran out, picks and shovels scaled to modern day giants that long outlived the rush. Levi Strauss’ denim trousers have since clothed over a billion customers globally, while Wells Fargo’s express delivery and banking services grew into the financial multinational we see today. Whether photonics, whole wafers, or neoclouds are the next big innovation is anyone’s guess, as only time can distinguish between structural defensibility and hype-fuelled CapEx cycles. Customer concentration, geopolitical risks, and supply chain fragilities are still very real risks. The question remains: Will trillions translate to progress, or are we all inflating a bubble digging for fool’s gold?

Sources

https://howtoarchitect.io/three-companies-93-and-the-memory-wall-nobody-saw-coming-19a50d0feaf4

https://mlq.ai/research/lumentum/

https://vessl.ai/en/blog/what-is-a-neocloud

https://www.coreweave.com/blog/a-defining-year-for-the-essential-cloud-for-ai

https://nvidianews.nvidia.com/news/nvidia-and-nebius-partner-to-scale-full-stack-ai-cloud

https://www.fool.com/investing/2025/10/19/the-newest-artificial-intelligence-stock-has-arriv/

The CAINZ Digest is published by CAINZ, a student society affiliated with the Faculty of Business at the University of Melbourne. Opinions published are not necessarily those of the publishers, printers or editors. CAINZ and the University of Melbourne do not accept any responsibility for the accuracy of information contained in the publication.